Morgan Stanley's Q2 2025 Swiss Watch Market Report

Analysis of Key Trends, Challenges, and Opportunities for Watch Brands and Watch Collectors from Q2 2025

I am well aware I have been posting a lot about business/finance and not much about psychology - I had hoped to correct this imbalance in my next post, but then this report was published and it derailed that plan! I will try and make this as short as possible (since a lot hasn’t changed since Q1 2025 anyway).

Estimated reading time: ~15 mins

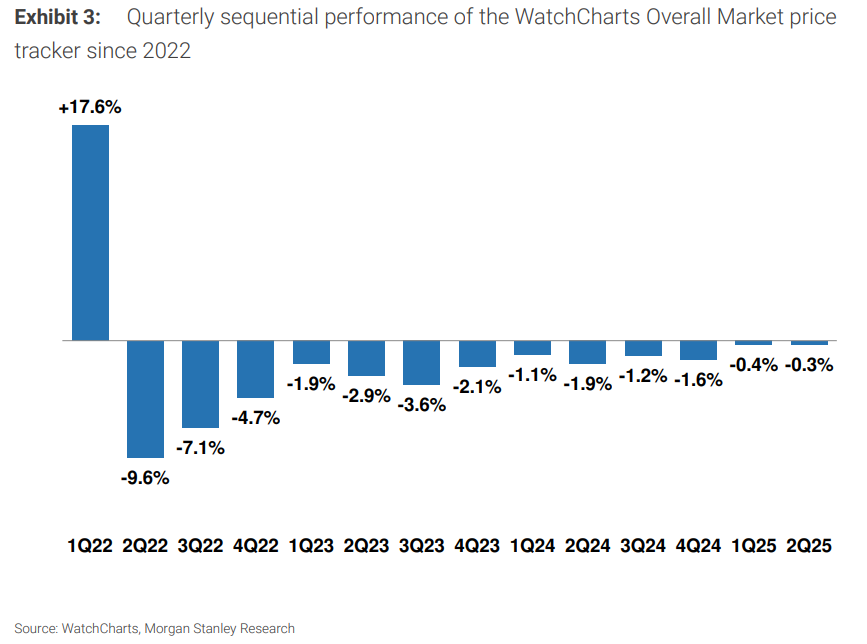

I will begin with a quote from my post about last quarter’s MS Report: “Until next quarter’s report, when we’ll undoubtedly be discussing yet another -0.something% decline...” and add the following quote from this quarter’s MS report: “Overall, prices of watches on the secondary market continued to decrease in 2Q, for the thirteenth quarter in a row.”

That’s the story, and we really ought to leave it at that, because I struggled to extract any juicy insights from this quarter’s report… but I went ahead with this post because there are many new subscribers who may not have seen the previous quarters’ updates. If you’ve been following these for a while, this will all seem like déjà vu (again!).

ScrewDownCrown is a reader-supported guide to the world of watch collecting, behavioural psychology, & other first world problems.

Ok so, looking back, if Q1 2025 was about “cautious optimism” with a -0.4% decline (which was an improvement from Q4’s -1.5% drop), then Q2 2025 is perhaps best described as… “in limbo due to tariffs.” The WatchCharts Overall Market Index managed just a -0.3% quarter-on-quarter drop which may be the smallest drop since Q2 2022, but is still not a recovery. All this quarter demonstrated was how a handful of blue-chip brands can prop up an entire market while everyone else is scrambling to survive. When you strip away four big brands (Rolex, Patek, Cartier, and Omega), the secondary market looks more like a charity case than a luxury goods sector.

That’s the long and the short of it; below I will lay it all out in sections for the nerds.

Disclosure: WatchCharts provides all the data in the report. They don’t pay SDC for advertising, and SDC does not pay WatchCharts for this report. Since they're kind enough to share, and I enjoy bringing readers fresh info - I am happy to recommend you check out their website here.

Not an affiliate link, but if you want a discount or a free trial, send a DM to Hamza Masood - he may or may not oblige, and I didn’t ask for permission to write this here 😂

Key Findings

These are the main takeaways from the quarter (charts shared in the sections below):

The WatchCharts Overall Market Index dropped -0.3% quarter-on-quarter. Yes, this was an improvement from Q1’s -0.4% decline, but it still marked the 13th consecutive quarter of declining prices. The “stabilisation” narrative only holds if you ignore the fact that 29 out of 35 brands posted negative performance.

Four brands carried the entire market. Rolex (-0.2%), Patek Philippe (+1.1%), Cartier (+0.9%), and Omega (-0.1%) were the only reasons the overall index didn’t evaporate. Without these four, the market would have looked like a proper disaster.

Listed groups continue to struggle. LVMH (-3.1%) and Richemont (-2.4%) both posted disappointing numbers, and Swatch Group (-1.1%) was saved entirely by Omega’s stability.

Retail price increases across the board. Every single tracked brand raised US retail prices - from Tudor’s digestible 2.5% to Patek’s criminal 6.9%. It seems the 10% US tariff increase that hit in May forced brands to pass costs to consumers which smacked value retention even harder.

Vacheron Constantin hit record lows. The former COVID-era darling now sports a value retention discount exceeding 40% - this is a record low, apparently.

Secondary Market Trends

I previously said Q1 2025’s -0.4% decline was an improvement, so I suppose it is only fair to say Q2’s -0.3% decline continues this glacial pace of “improvement,” but the year-on-year comparison tells the real story:

Q2 2025: -0.3% vs Q2 2024: -1.9%

Q1 2025: -0.4% vs Q1 2024: -1.1%

Q4 2024: -1.6% vs Q4 2023: -2.1%

So yeah, things are less sh1t than they were a year ago, but that’s like saying a broken leg is better than a broken spine - it’s a true statement, but you wouldn’t celebrate either!

The other point is the polarisation I mentioned in Q1 has only intensified. Four brands are doing the heavy lifting while the rest of the market burns. From what I can tell - and the report seems to align with this view - this is creating a two-tier luxury watch market where the rich get richer and everyone else fights over scraps.

Group Performance

That brings us to the performance by major groups, and of course, this is where it gets most interesting. I often think about it like the luxury watch market is a game of musical chairs, and all these brands are wondering when the music’s about to stop - i.e. which brands will fall out of favour with consumers.