Morgan Stanley's Q3 2025 Swiss Watch Market Report

Analysis of Key Trends, Challenges, and Opportunities for Watch Brands and Watch Collectors from Q3 2025

Another quarter, another report from Morgan Stanley… but for once, there is some interesting stuff to talk about. After thirteen consecutive quarters of decline (more than 3 years of watching prices fall) the WatchCharts Overall Market Index has finally turned positive - it’s up +1.5% quarter-on-quarter. Obviously there’s more to this than meets the eye, and this might just be a perfect storm of confusion with the 39% US tariff on Swiss goods that landed in August 2025, plus the recent round of aggressive retail price increases.

I guess everyone is wondering whether the Q3 surge in secondary demand is real, or was it just panic buying before prices were adjusted?

Estimated reading time: ~14 mins

Quick fun fact: Patek is now most expensive to buy in the US, but Rolex, Omega and Cartier are still more expensive in the UK than anywhere else.

Disclosure: WatchCharts provides all the data in the report. They don’t pay SDC for advertising, and SDC does not pay WatchCharts for this report. Since they’re kind enough to share, I am happy to link to their website and recommend you check it out. (Not an affiliate link)

Key Findings

Here are the main takeaways from the quarter (charts shared in the sections below):

The WatchCharts Overall Market Index rose +1.5% quarter-on-quarter. This was likely driven by a few specific things; the 39% US tariff introduced in August, retail price increases, and buyers rushing to purchase before prices adjusted further.

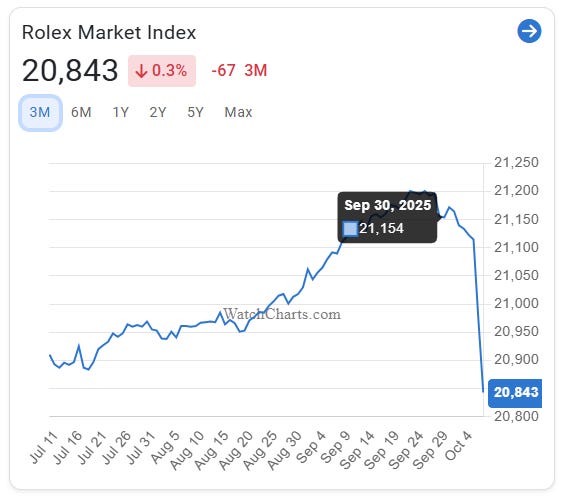

Side note: since the quarter closed (not in the report), the index is already down by -0.5%!

Patek and Rolex drove the gains, but it’s complicated. Patek spiked +3.9% QoQ (and +3.3% YoY), and Rolex posted +1.3% QoQ (+1.0% YoY). These were the only two brands showing year-on-year growth, but Patek’s rise was driven by panic buying ahead of a loopy +15% retail price increase, and we’ll likely see the hangover in Q4 or Q1 next year.

Listed groups continue to struggle. Richemont (-1.7%) and LVMH (-1.0%) both posted declines, and Swatch Group (+0.5%) was saved by Omega’s +2.0% rise. The pattern from the past two years is mostly unchanged, and private players outperform, while listed groups underperform.

Another round of savage retail price increases. After every tracked brand raised prices in Q2, five did it again in Q3. Patek led the carnage with a +14.9% increase, followed by Cartier (+8.1%), Omega (~+8%), Tudor (+4%), and IWC (+0.4% average). That’s 25%+ cumulative increases for Patek in less than a year. Brands are clearly trying to offset the 39% tariff, but of course, destroying value retention in the process (that’s kinda “baked in to the definition” here). It also didn’t help that the USD/CHF rate also added to their woes:

Patek’s value retention dropped below zero. For the first time in over three years, Patek watches now trade below retail on average, falling from +5.6% in Q2 to -4.7% in Q3. Combined with similar drops in Q1 and Q4 2024, Patek has lost more than 24 percentage points of value retention (VR) in just nine months - no surprises there, because that kinda lines up with their +25% cumulative price increases for 2025. That said, this is more of a bifurcation; sports models still have decent VR, while the rest are now negative.

Rolex stands alone. At +15.7% above retail, Rolex is now the only brand whose watches trade meaningfully above retail, and again, they also happen to be the ones who didn’t go ape sh1t with the price increases. AP is clinging to positive territory at +1.6%. Beyond the Big Three, every single brand trades at discounts exceeding -31% to retail, with Vacheron languishing at -43.9%.

Another side note: since the quarter closed (not in the report), Rolex is already down by -1.47% as well.

Secondary Market Trends

This quarter has ended a streak of thirteen consecutive quarters of decline. Here’s how we got here: