Richemont is Cartier, Cartier is Richemont. Everything Else Is a Hobby.

Morgan Stanley reverse-engineered the brand numbers from Richemont; Cartier and Van Cleef earn more than 100% of the profit; the watch division's margin is 1.2%

Most SDC readers will be familiar with the usual Morgan Stanley (MS) watch reports. A few times a year they publish various Swiss-watch market reports, I then summarise the secondary-market carnage, I make a joke about how a broken leg is better than a broken spine, and we all move on. Those reports are mostly about prices i.e. what your watch is worth on the grey market.

Today’s report is a little different; MS recently published a “Foundation” report on Richemont which is intended to inform MS clients who might be thinking about buying Richemont shares. The analysts open the report with this paragraph:

I mean, this is hilarious false modesty because the paper is stuffed with estimates. As for SDC readers, the reason you might find it interesting is that Richemont does not publish brand-level numbers. They mostly report in three buckets (Jewellery Maisons, Specialist Watchmakers, and “Other”) and that’s that. They used to break out Montblanc but stopped in 2013.1 So when you ask “how much money does IWC make?” or “is Jaeger-LeCoultre profitable?”, the answer has always been soething along the lines of nobody knows.

And I suppose even after reading this we still don’t ‘know’ anything for sure, but this report is MS’s best attempt at reverse-engineering those numbers. They are most likely wrong… but given these are estimates built from channel checks, export data, and 20 years of watching the company, it’s as good as we might get.

Not investment advice - obviously.

Estimated reading time: ~18 minutes

Richemont is Cartier, Cartier is Richemont

If you’ve watched Ace Ventura, you’ll recognise the reference above… and if you haven’t, you must watch it ASAP but, I digress…

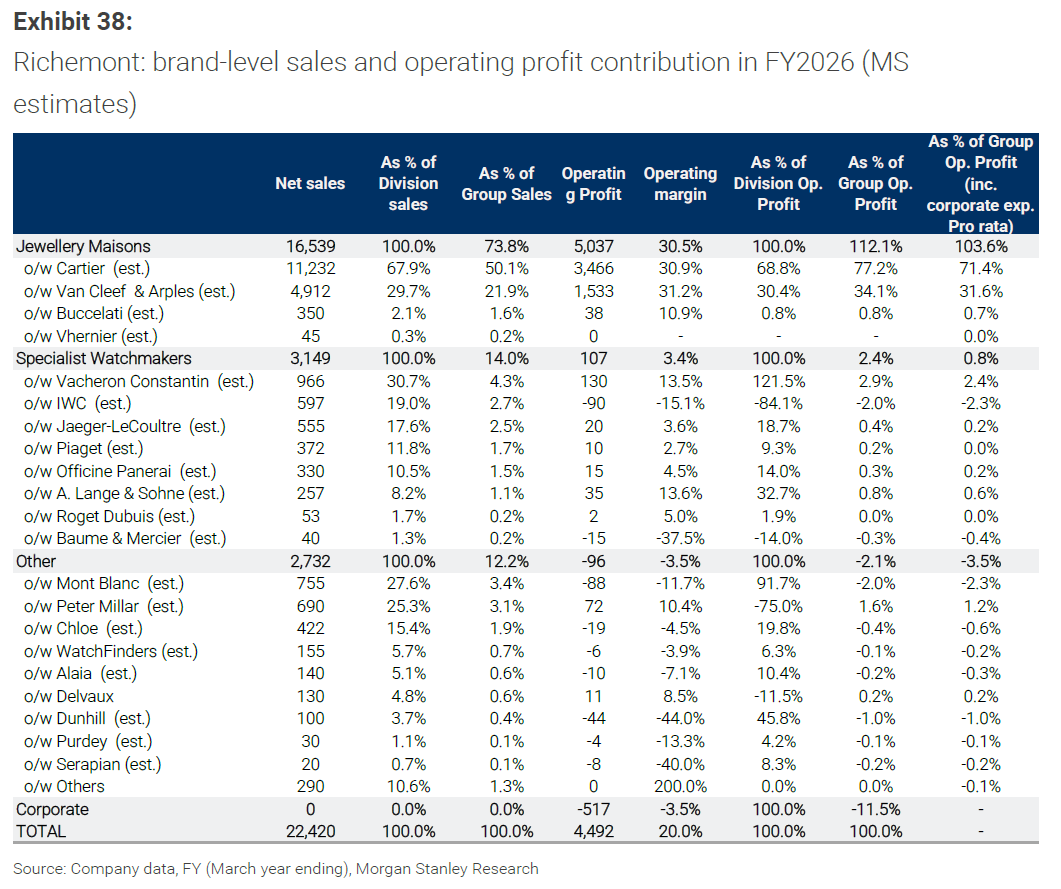

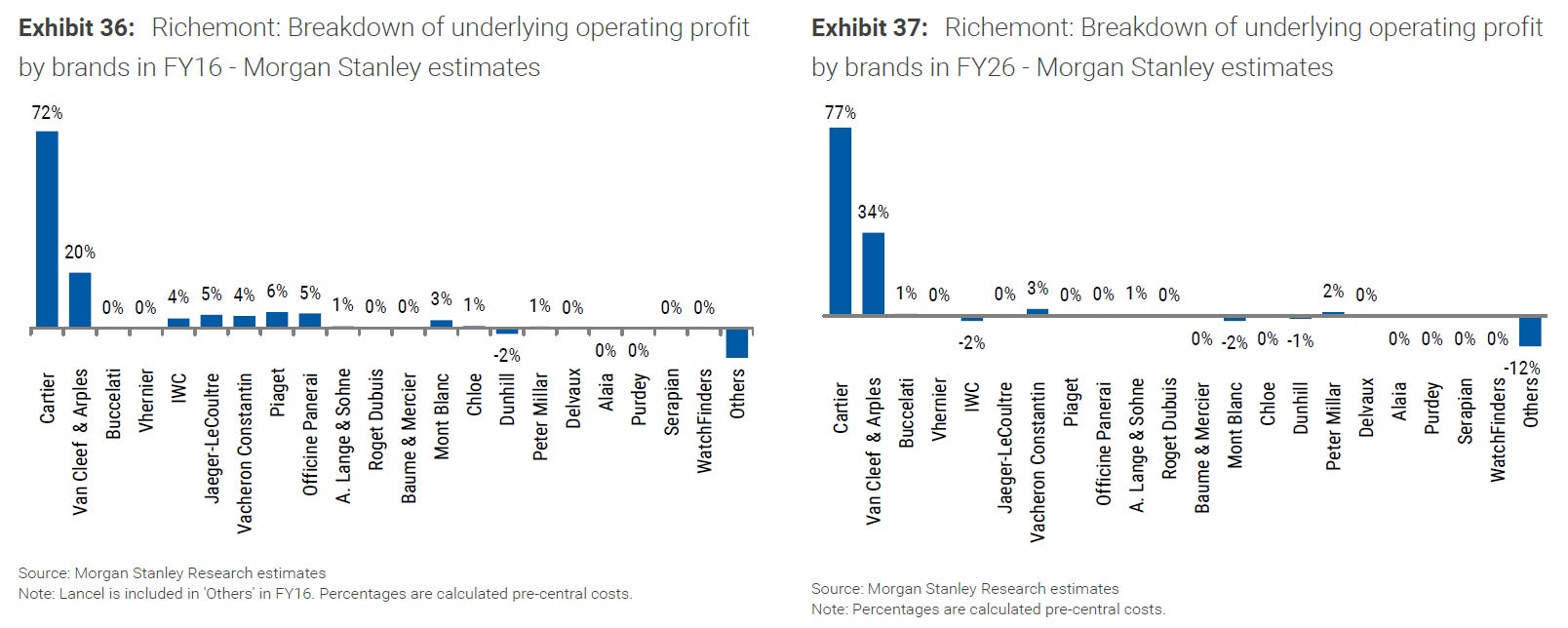

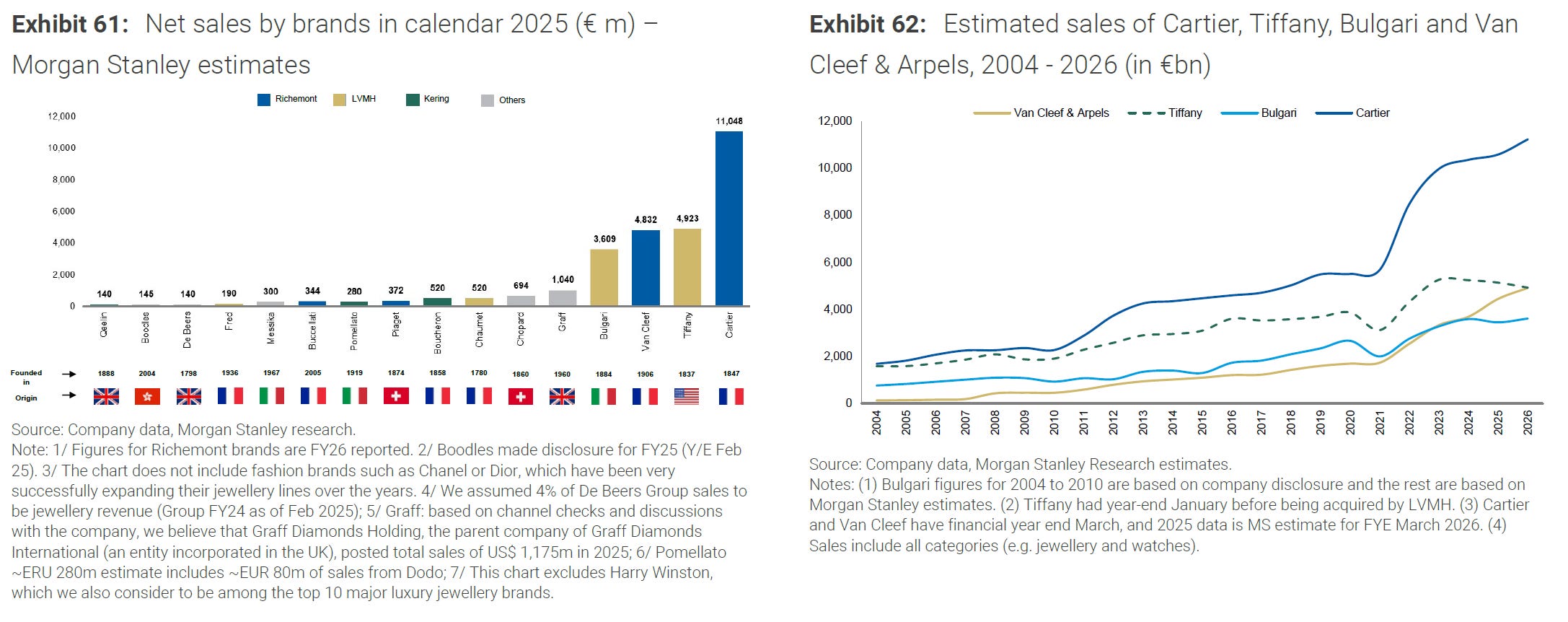

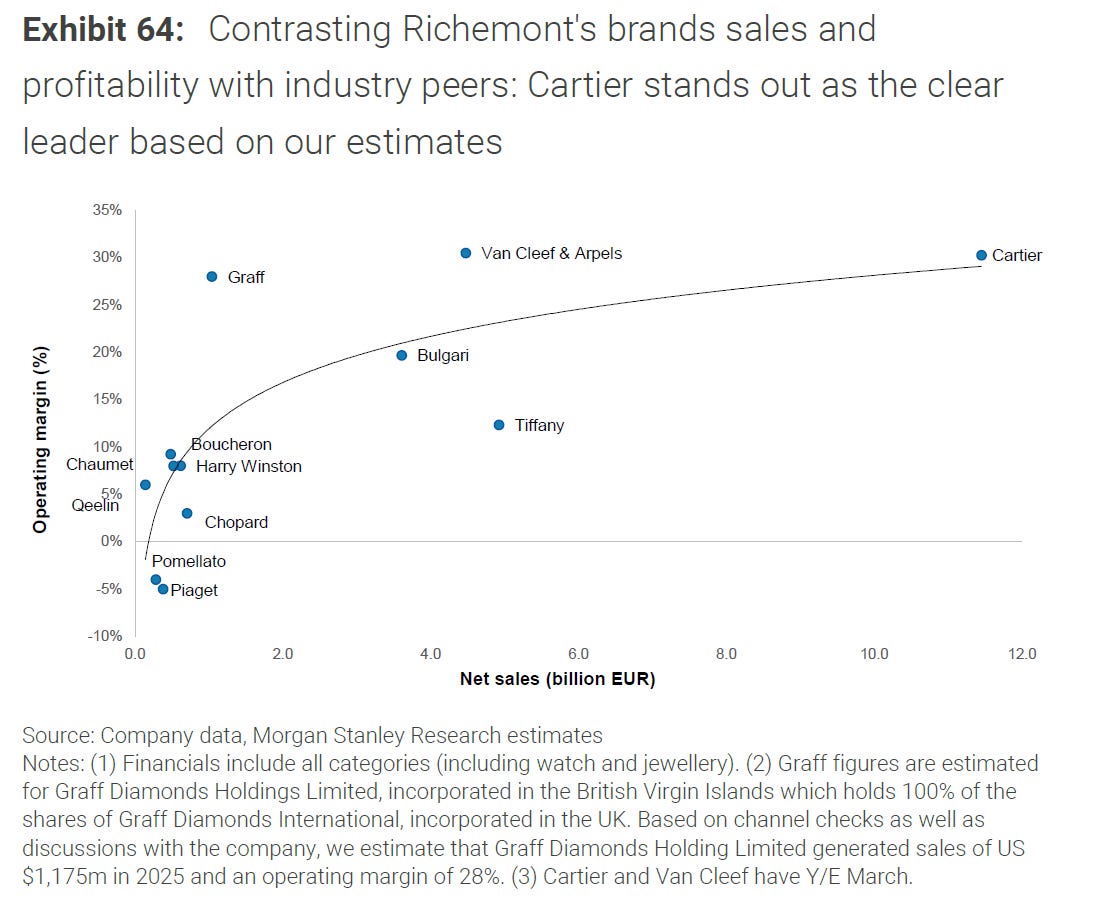

For the year to March 2026, MS estimates Cartier did about €11.2 billion of sales and ~€3.5 billion of operating profit - that’s a ~31% margin. Contrasting against the group, Cartier alone is roughly half of Richemont’s sales and about 77% of its operating profit (call it ~71% once you load it with its fair share of head-office costs); basically it’s one brand responsible for ~75% of the profit.

Then if we add Van Cleef & Arpels - ~€4.9bn of sales, ~€1.5bn of profit - these two together make up about 72% of group sales and more than 100% of group operating profit. “But wait”, I hear you say… “how can two brands earn more than 100% of the company’s profit?” Well it’s really simple… everything else, in aggregate, loses money (or close to it).

The watch division barely breaks even, the fashion-and-leather “Other” division has been loss-making for the better part of two decades, and head office burns roughly half a billion euros a year on top.2 In short, Cartier and Van Cleef earn the profits, and the rest of the empire just burns the lot like a billionaire’s deadbeat child might do.

You know how a holding company sometimes turns out to be one good business carrying a portfolio of shitters? One might argue Berkshire Hathaway is GEICO-and-friends, and a lot of media conglomerates are really one cable network funding a dozen vanity projects... heck, SpaceX is basically Starlink + AI dreams, right?

Well, Richemont is essentially a jewellery company (Cartier + Van Cleef) that happens to own eight watch brands, a German pen-maker, a French fashion house, and - I am not even making this up - an American golf-apparel label.

The jewellery is basically paying for a bunch of side-hobbies.

Specialist Watchmakers Division

Side note: there is a problem in the report with the operating profit and the operating margins… you will notice they are not identical in the various tables - Exhibit 38 vs 83 - seems like someone copied the wrong tables into the report, but the variance is negligible so we’ll go with it. MS was contacted for an explanation, but they have not responded.

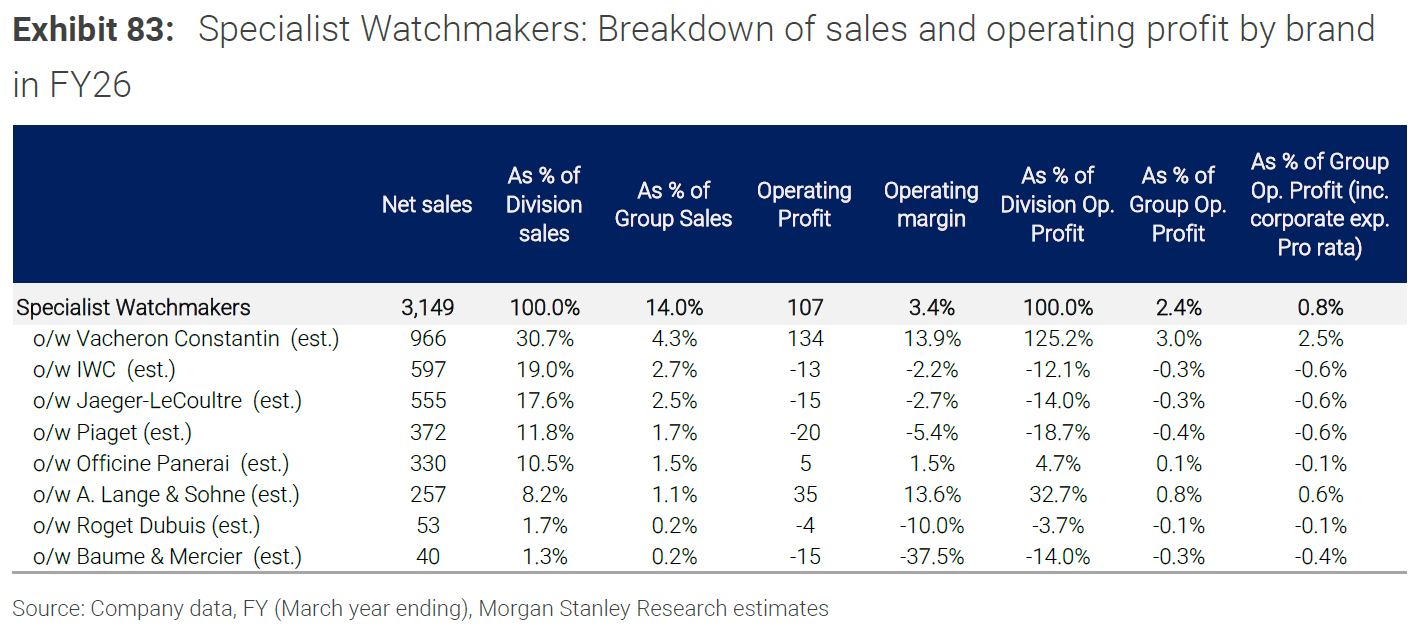

Richemont’s “Specialist Watchmakers” division (does not include Cartier, whose watches are counted in Jewellery Maisons) did €3,149m of sales in FY26 and €107m of operating profit. That supposedly translates to a 3.4% operating margin. For context, this same division reached 27% margin at its peak back in FY13. It has fallen off a cliff in the last two years especially. After you allocate central costs, MS reckons the division’s true margin is something like 1.2%… on some of the most storied names in horology!

Vacheron Constantin makes up ~€966m (or ~31%) of this division’s sales; ~€134m of this is operating profit, which is actually ~125% of the whole division’s operating profit. Lange is the second-best earner, with a decent 13.6% margin on ~€257m of sales. And then… the rest make almost no money… except for IWC which actually loses money.

So what we see here is that some of the most storied names in watchmaking history - IWC, JLC, Panerai, Roger Dubuis and (on a good day) Piaget - are, on these estimates, together running at a loss inside one of the richest luxury groups on earth.

Taken together, they are not even “growing slowly” or “running below their potential”… they are outright losing money (I am taking them together, because if you add up the small operating profits, the IWC loss is still too large to be offset). If these were standalone companies, you would be reading headlines about restructuring, acquisition, or in the case of IWC, maybe even bankruptcy. But here, because they’re protected inside Richemont, the losses get absorbed by Love bracelets and nobody has to explain themselves on an earnings call.3

Data dump

Now let’s move on to the juicy numbers like volumes and average selling prices.

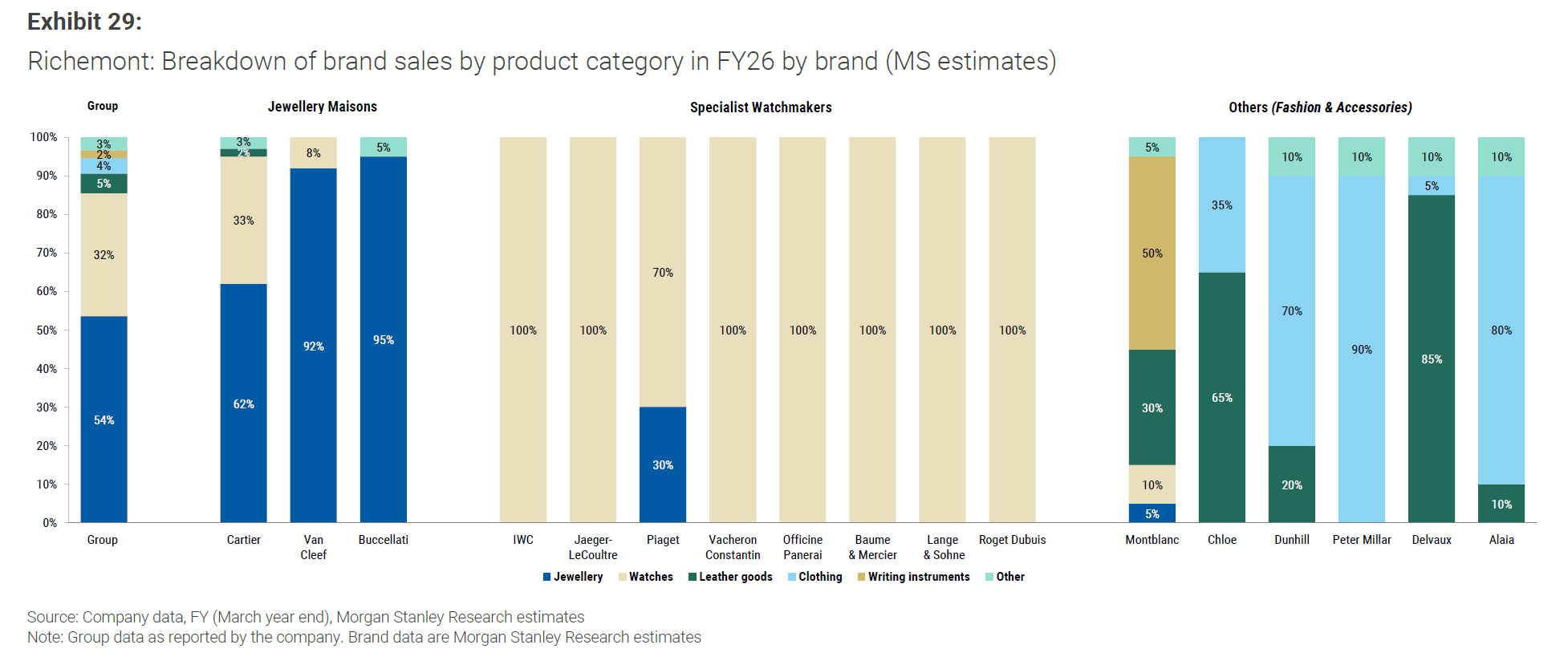

Cartier: ~695,000 watches, ~€3.65bn of watch sales. That makes Cartier the #2 watch brand in the world by revenue, behind only Rolex and ahead of Omega. Isn’t it ironic that the biggest watch brand in Richemont isn’t even in the watch division? We already knew Cartier was the hero but seeing it laid out against the “specialist” watchmakers is something else.

IWC: ~118,000 watches, ~€597m.

Jaeger-LeCoultre: ~78,000 watches, ~€555m.

Panerai: ~38,000, ~€330m.

Piaget: ~30,000 (watches only), ~€372m total sales (Piaget is ~30% jewellery).

Vacheron Constantin: low tens of thousands of units, ~€966m.

A. Lange & Söhne: ~5,200 units, ~€257m.

When you calculate price per watch, you have to separate “what the brand books” from “what you pay at retail.”4 Roughly, Cartier books a bit over €5,000 per watch (retail closer to ~€7,500). IWC books a bit over €5,000 too (retail ~€7,800). Vacheron books something like €45,000 per watch - basically retail, since Vacheron sells a lot through its own boutiques now.

So in short, IWC sells ~118,000 watches to book ~€600m. Vacheron sells maybe a sixth of that volume to book ~€1bn. One brand is a volume business priced like an accessible-luxury name; the other is a scarcity business priced like a Patek alternative. Guess which one makes money? (Yes I know you already saw the table - Vacheron’s 13.9% margin versus IWC’s loss.) This is the the whole “high volume, low price, low margin” story in black and white.

And then there’s the pricing problem which makes sense to nobody - not even MS - and they flag it; that the entry price into Jaeger-LeCoultre (steel Reverso) is around €6,500, and the entry into Cartier (steel Tank Must) is around €3,500. JLC’s cheapest ‘serious’ watch is roughly double Cartier’s, and MS reckons this is “difficult to justify.” I’d agree.

In fact, I’d go even further; I’ve mentioned before, the watch industry has been abandoning the lower price points altogether and raising prices on the existing mix - if you keep squeezing the people who are already keen on the brand, and price out anyone new who might come through the door, nothing good is likely to happen. Cartier at least kept a foot in the door at ~€3,500 and it is now the #2 watch brand on earth. JLC priced its entry watch at double that, missed the sports-watch boom, struggles to sell their rectangular watches in China, and is now losing money. The Tank Must is kind of like a ‘recruiting tool’ for the brand, and the steel Reverso is more akin to a velvet rope outside an empty nightclub.

As you’d expect, only one of these strategies is working.

Why the watch division is dying

So why is the margin 3.4%?

First, fixed-costs are a bitch. Over two decades, Richemont vertically integrated its watch brands - that is, they were building movement and case manufacturing upstream, and buying up retail downstream. That’s essentially a high-fixed-cost setup, and it works well when sales are growing because you spread those high fixed costs over more units (operating leverage - the same thing which makes software companies so profitable at scale). But the division’s sales peaked around FY16 and have been flat-to-down in euros ever since. High fixed costs + flat sales = the whole thing runs in reverse, and your margin collapses. And hey, shocker, this is what the chart shows… 27% down to 3.4%.

Second comes down to the stores. Look at IWC; in FY16 it had 86 boutiques and did ~€700m. By FY26 it had 238 boutiques and did ~€600m. They nearly tripled the store count and revenue went down. Essentially, this speaks to a growth plan that never came true. (Montblanc is the same sort of thing; peak ~€980m in FY19, ~€760m today, loss-making, with a store count that blew up and is now being cut back.) MS suspects “high rental costs in prime locations and, in some cases, relatively low sales productivity.” In other words, they signed a lot of expensive leases on the assumption the watches would fly off the shelves, and then they didn’t.

Third is scale. The three big Swiss groups aren’t that different in total market share -Rolex ~34% incl Tudor, Richemont ~18%, Swatch ~16%. Ok, Rolex is running away with it, but with the group numbers it still looks respectable. But then, when you cosider brand share, the Rolex brand alone is ~33% of the entire Swiss watch market. None of Richemont’s watch brands, excluding Cartier, has a share above 3%.

This is the secret sauce I suppose; Rolex makes >30% margins because it makes over a million of essentially the same handful of watches, with all the purchasing power, manufacturing efficiency, and brand gravity that sort of scale will buy you. Richemont’s watch division is eight sub-scale brands in a trench coat, each carrying its own movement R&D, its own marketing, its own boutiques, its own everything. What’s worse, none are big enough to gain any meaningful operating leverage. A simple example is to consider the difference between one factory making a million widgets and eight workshops each making forty thousand; the unit economics won’t even get close.

This connects straight back to The Decay of Luxury Watchmaking and the “80% solution.” Everyone wanted the prestige of an in-house manufacture; everyone built the capacity; and now Richemont is sitting on a pile of sub-scale, vertically-integrated, high-fixed-cost watch brands in a market that’s polarising toward a handful of giants. The Big Four (Rolex, AP, Patek, RM) went from 37% of the market in 2019 to 51% in 2025. The rich got richer and the sub-scale heritage names got squeezed. Within Richemont itself, MS reckons only Vacheron and Cartier gained share over that period.

This is like musical chairs, and their watch division has eight brands fighting over one chair!

Iconic-line economy

MS estimates that at Cartier, the Love, Trinity, and Juste un Clou lines together generate more than 75% of the brand’s jewellery profits - with Love the single biggest contributor. Love, the bracelet you screw onto your wrist, is the biggest jewellery line in the world (over €1bn in sales), and MS estimates its gross margin exceeds 75%. But seriously, in general, Cartier is a monster of a business… just, wow:

At Van Cleef, it’s even more concentrated; the Alhambra line (bracelets that start around $4,000) accounts for about 60% of VC&A’s profits. The brand has been trying for 15 years to reduce its dependence on that one motif (the Perlée line launched in 2010) but it’s still less than 10% of profits. In the end, Van Cleef is, albeit profitably, a one-clover pony.

Both empires are built on the accessible lines, and not the high-jewellery showpieces. Van Cleef can sell you a high-jewellery necklace north of $1m - but the profit engine is the $4,000 Alhambra bracelet. The reason is that once a design becomes instantly recognisable, you’re no longer selling gold and stones, but recognition. A Love bracelet at >75% gross margin has nothing to do with the cost of material - these are priced off the fact that everyone at dinner knows exactly what it is and roughly what it cost. MS makes the point that jewellery, unlike handbags, can’t lean on logos and monograms, so a handful of brands solved the ‘recognition’ problem with iconic shapes instead - and in the age of Instagram, instant recognisability is all you really need.

Now apply that logic to watches; Cartier’s watch business works for the same reason its jewellery does! It has a few hyper-recognisable shapes (Tank, Crash, Santos, Ballon Bleu, Panthère) sold at accessible-to-mid prices, where you’re buying the silhouette, not the movement. Cartier “stopped trying to be a quasi-Patek a long time ago,” as I said before, it sells design, not horology… and it sells it cheaply enough to recruit new customers into the fold.

Now look at the loss-makers; these are brands trying to sell horology (movements, finishing, technical credibility) at high prices, to a market that wants to buy recognition. JLC has arguably the deepest technical bench in Switzerland and MS calls it “one of the industry’s most admired manufactures but arguably one of its most under-monetized.”

That is JLC’s problem at the end of the day; technical excellence is not what’s being monetised right now - recognisable shapes at accessible prices is apparently where it’s at. Cartier seems to have figured that out, and the other specialists are still selling stuff the market doesn’t seem to be willing to pay a premium for.

What’s working in watches

There’s a bright spot in the watch division, though. Under Louis Ferla (CEO 2017–2024), Vacheron went from ~€380m to over €1bn in revenue. Turns out, Ferla didn’t try to out-hype AP or Patek. All he did was sharpen their positioning around heritage, elegance and exclusivity, leaned hard into the Overseas as a Nautilus/Royal Oak alternative during the sports-watch boom, pushed pricing discipline using DTC boutiques, and drove the average selling price up by piling into high complications and unique pieces. By 2023 Vacheron was selling watches at an ASP near CHF 39,000, and revenue grew much faster than units. It’s the only Richemont watch brand besides Cartier to gain share over 2019–2025, and MS calls Ferla’s tenure “one of the most successful luxury watch brand transformations of the past decade.” So what did Richemont do with its best watch-brand operator? Made him CEO of Cartier in 2024.