Watch collecting and the winner's curse

How information asymmetry leads to poor purchase decisions

You’ve probably overbid on a watch at some point… Maybe you knew it at the time; maybe you only realised weeks later when the dopamine wore off. Either way, there’s a name for what happened to you - and it was first identified by oil companies haemorrhaging money in the 1970s.

The Winner's Curse

The winner’s curse is a famous empirical phenomenon in common value auctions, first described by Capen, Clapp, and Campbell (1971). These authors showed that oil companies had to report a drop in profit rates because of systematic overbidding in oil lease auctions. Volumes of experimental evidence for the winner’s curse has since been published, so I’ll leave you to look those up for yourselves if you’re curious.

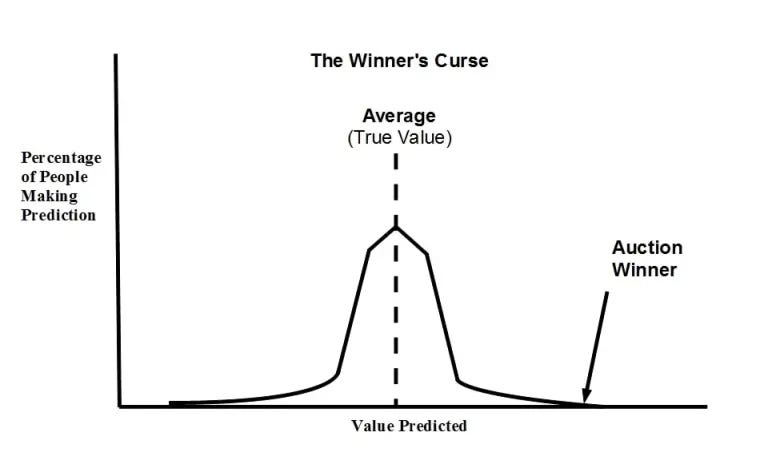

To make this easier to understand, let’s assume Aurel is auctioning off a box containing exactly £25 worth of various coins. N people participate in the auction, and nobody can examine the coins in the box before the auction. These N people can simply look at the open box full of coins, and try and estimate the total worth of the coins contained within. After completing their evaluations, all the people submit a bid to buy the box and its contents.

Everyone is hoping to make a few quid, however, it may be the case that one of them overestimates the value of the coins in the box. As a result, that person may bid too much into Aurel’s auction. If this happens, that person may, depending on the auction dynamics and the other bids, end up paying Aurel more than the value of the coins contained within the box.

It turns out that the winner of Aurel’s auction will end up overpaying for the box of change much more frequently than we would otherwise expect; and this is the winner’s curse.

To see how this works, let’s denote the ith bidder’s valuation as follows:

Vi=25+ϵi where ϵi is the error each bidder makes in their valuation.

The highest valuation of the box of coins among N bidders will be: max(V1,...,VN) = 25 + max(ϵ1,...,ϵN).

In plain English… each person’s guess equals the real value, plus however wrong they are. The winning bid almost always comes from whoever was most wrong in the optimistic direction.

Which means, this highest valuation is very likely to be larger than £25. To see why, let’s assume all bidders are equally likely to overestimate the value of the coins, as they are to underestimate it. In this case, for the highest valuation to be less than £25, all N bids have to underestimate the value of the box of coins. This happens only 1/(2^N) of the time!

So if ten people bid on Aurel’s box, the odds that every single one of them undervalues it (meaning the winner somehow bags a bargain) are roughly 1 in 1,024. Put differently, in about 999 out of 1,000 auctions, the winner will have overpaid. Those are terrible odds, and yet people queue up for auctions all the time!

Also, the discussion of the highest valuation is important because, typically, the person with the highest valuation will win the auction. Let’s call this person with the highest valuation, whom we expect to win the auction, JC Biver. If JC Biver wins the box of change and tallies up the money, he’s probably in for a nasty surprise. Almost every time, the box will have less money than he anticipated it having. Many times, this effect is so pronounced that not only will JC Biver have not made as much profit as he had anticipated, he will have lost money!

Just like that, JC Biver has fallen victim to the winner's curse!

The watch connection

When it comes to the winner’s curse, we can spend hours reading about biases and the impact of information asymmetry in auctions. Moser (2018), did an experiment where he had two stages of bidding, and in the second phase he revealed whether the bids in the first phase were winning or not. He found that after being provided with the information at the end of stage 1, these bidders were more likely to avoid the winner’s curse.

Perhaps more interestingly, he found that information can also be negative for the bidders in certain contexts. The subjects in the experiment imperfectly differentiated between situations where adjusting a bid was rational and situations in which it was irrational... and they often used simple heuristics instead of making strategic changes.

He suggests that this behaviour could possibly be explained by the “joy of winning” or “disappointment of losing.” What he observed was when subjects lost an auction in stage 1, most of them increased their bid in stage 2, regardless of their own evaluation of value. On the other hand, when they were told that they had won an auction in stage 1, they acted more strategically and aligned their bids with due consideration given to their own value assessments.

Just think about what happens when you lose out on a watch at auction. The rational response is to reassess whether your valuation was right, no surprises there; but the emotional response (the one most of us actually have) is to consider how much higher to bid next time. You’re not updating your estimate of what the watch is worth - you’re actually just trying harder to win. That gap between rational and emotional is exactly where the winner’s curse lives.

Hopefully this short analysis will encourage you to do your own literature review and if you do, I would welcome a further discussion on the topic. With the above in mind, I'd like to conclude with my takeaways, in relation to watches.

Grey market is a permanent auction

The winner’s curse was first studied in formal auctions, but don’t assume you need a paddle and a numbered card to fall victim to it. Every time you buy a watch on the secondary market, you’re essentially entering an auction - you’re simply competing against buyers you can’t see.

When a dealer lists a watch at a particular price, that price reflects what the dealer believes to be the highest amount someone in the market might be willing to pay. If nobody else would pay that much, the watch would still be sitting there, and the price would drop. So by definition, the person who buys it is the person with the highest valuation. And as we’ve just established, the person with the highest valuation is statistically the most likely to have overestimated.

This applies to AD waitlists too, by the way. When you accept a watch from an AD after a long wait, you might feel like you’ve “won” because you got the call! But the true cost isn’t just the retail price. It’s the relationship management, the complementary purchases, the time spent, and the opportunity cost of the capital you kept liquid while waiting. Add all that up, and you might find you’ve paid more than the grey market price you were trying to avoid.

Conclusion

I picked the above paper because it provided the simplest actionable conclusions... so I concede, this conclusion may well suffer from some selection bias. That said, you are smart, so hopefully you will read this with a pinch of salt.

Clearly the presence of information is the key to avoiding the winner’s curse. This is hardly a surprising statement, but it deserves some further probing. When you’re buying a watch (whether at auction, or not), you are taking all the information you have available, and then computing what you think is a fair price to pay. This includes things like asking friends’ opinions to determine the ‘status value’ , how badly you need some dopamine from a new watch, or maybe even how happy you think the watch will make you because it's a lifelong ‘grail’ pursuit.

Aside from this, you’ll also factor in things like the resale value, or rarity, which will determine whether a watch might retain some future value. All of this data is a mixture of facts, rumours, and unquantifiable subjective nonsense. In the above example with Aurel, we called this ϵi – the error each bidder makes in their valuation,

What seems to be happening in the watch world today is an overinflation of what I described above as unquantifiable subjective nonsense. This leads to mini-frenzies, such as the recent rise in value of the Rolex OP Tiffany. While there are buyers who are happy to undergo a willing suspension of disbelief, simply to participate in these frenzies... the sensible ones know better.

If you’ve read a few of my previous posts, you will know about how I frequently warn against the impact of social media on your purchase decisions. In this case, social media is just one of your sources of information. You might observe a collector who has a ‘track record’ of getting in early with today’s hottest brands... you might see influential accounts promoting a particular reference... all of this feeds into your subconscious calculations, probably without you giving it much thought. A simple example is the recent spike in ‘advocacy’ for DeBethune, Czapek and others ... try and think more critically as you scroll through your feed, and I bet you’ll notice it immediately.

Is this wrong? Of course not. Will it influence your future buying decisions, or evaluation of options? Absolutely! That’s what social media is designed to do, and that is pretty much how the term influencer was coined. So while this isn’t news to anyone, the point I am driving at is you ought to reduce the weight you place on social media and seek other sources of information. Try and visit manufacturers, seek advice from friends who own these watches (rather than self-serving influencers on Instagram), and try to get hands-on with the watches to gather your own primary information.

All this will hopefully equip you with better information, enabling you to more accurately value any future purchases, and make sure you don’t fall victim to the winner’s curse when you do pull the trigger on your next piece.