SDC Weekly 142; Nautilus - the 50-year-old porthole; Georges Kern on Universal Genève; Dominique Renaud - building a village around a genius

Plus a Singapore watch Ponzi, the rise of Jacob the Watchmaker, the hunt for Satoshi, white-collar sweatshops, an essay on unfolding, what a spider dial can teach you about parenting, and more!

🚨 Welcome back to SDC Weekly! Everyone and their dog will be in Geneva this week talking about all the novelties, so I am glad to get this out on Monday before the storm. I won’t be in Geneva, so I probably won’t discuss any of the novelties. Should I just take the week off?

In case you missed it, I joined Tony Traina over at Unpolished Watches for a fun conversation which he published over the weekend (free for all):

Admin note: We handed this draft to the Unofficial Editor for review, but he took one look at our terrible grammar, started to Patek, and completely Philippe’d out. He stormed off muttering something about his time being too valuable, so we had to hit send without him. Please tap the title of this post or click here to read it online and see all corrections made after publishing.

If you’re new to SDC, welcome! If you have time to kill, find older editions of SDC Weekly here, and longer posts in the archive here.

Estimated reading time: ~45 mins

🤓 Building a village around a genius

Chris Hall went to visit Dominique Renaud at his new atelier in Tolochenaz, and the resulting dispatch was an interesting read. I came away with a few things I hadn’t really clocked before, and since one of SDC’s ongoing fixations is how indie brands actually stay solvent once the initial hype fades, this post was of particular interest.

The headline news, if you missed it, is that there is now an HHDR Group (Haute Horlogerie Dominique Renaud) sitting above both Dominique Renaud the brand and Renaud Tixier, and this company also holds a minority stake in Niton, and owns DS Assemblage which is a supplier that fell into trouble and was eventually acquired. If that sounds suspiciously like the Kari Voutilainen playbook of buying up the struggling suppliers you depend on, that’s because it is. Hall brings this up explicitly, and CEO Michel Nieto more or less cops to the strategy. Hall writes:

“…the entire point of HHDR Group is to lean on the prodigious creative output of Dominique Renaud while putting in place structures to ensure that the master watchmaker or inspirational engineer isn’t also having to balance the P&L, sort out the social media strategy and juggle retail relationships on four continents. What looked and sounded like an overabundance of corporate structures is really a framework for getting the best out of the team’s star talent, while also attempting to protect the various brands against shocks.”

What I found most interesting was the framing of all this. Nieto’s pitch, roughly, is that Renaud is a brilliant chap who should be left alone in the attic to invent things out of Lego Technic (yes, really - Hall even shared photos), while the grown-ups downstairs deal with P&Ls, retail relationships, and social media. The goal is to build “a village around him”, and the implicit point here, is that most indies collapse because the founder-genius ends up having to be the numbers-and-admin person too.

I also didn’t know - or had forgotten - that some of the patents Renaud developed over his career are still held by previous employers, meaning he literally cannot use his own inventions in his own watches until those patents lapse. The torque indicator on the Pulse60 is one that recently came back to him - which is its own little parable about what it actually means to be an “independent” watchmaker in 2026.

The question he ends on is whether this corporate-scaffolding-around-a-creative model is the future of sustainable indie watchmaking… I thought this was an interesting question to ask in the segment right now. Good job, Chris Hall.

🎤 Georges Kern on Universal Genève

Georges Kern recently appeared on Watch Advisor for an interview… Most of the Universal Genève segment will sound familiar by now, if you’ve followed all the press releases (here are a few: Fratello, Revolution, EuropaStar). The brand is positioned ‘in the middle’ of the traditional offerings and what you might call the bling merchants. Sizes are supposedly capped under 40mm (apart from the Dioramic I think) on the advice of an advisory board of vintage collectors whose brief from Kern was “tell me what not to do.” I thought it was impressive to see how multiple collections were launched at once (Polerouter, Compax, Cabriolet, Disco, Dioramic etc) and this helps ensure the brand doesn’t get labelled as a “Polerouter revival” effort. The whole UG operation is walled off in Geneva with its own team - distinctly separate from Breitling.

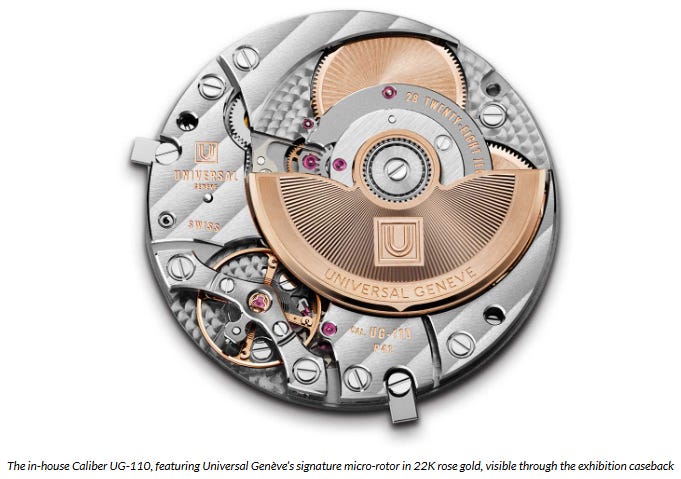

All of this is sensible, and most of it has already been dutifully written up by the watch press. The one bit nobody seems to have spoken about in much detail is where the movements come from. I mean, Revolution even went as far as calling it “in-house”:

LTM outsourcing

Well… Mr. Kern isn’t hiding anything… “LTM is producing our automatic … with the three former colleagues,” he says, almost in passing, “and we [Breitling] produce the chrono.”

LTM is Le Temps Manufactures, based in Fleurier. It’s a white-label specialist that serves roughly thirty brands from niche independents to major group-owned names and its speciality is small, high-end movements made in small batches for companies that want something better than Sellita without the capital expenditure of building a manufacture from scratch.

The UG-110 is, on all available evidence, a UG-designed calibre manufactured under exclusive contract at LTM. The integrated chronograph, Kern says, is produced by Breitling’s own manufacture. Velociphile, who is typically critical of most new movements, actually likes the new UG Polerouter movement - you can read his take here. I asked him who had hacked his account when I saw his essay - he laughed, and assured me it was still him 😂.

Anyway, none of this is particularly scandalous at all. This is how most of the industry works below the top tiers, and Vaucher, Kenissi, La Joux-Perret, and many others all run similar models. Some of the watches we all admire most come out of these sorts of arrangements. That being said, the gap between “Geneva-based independent haute horlogerie house with its own manufacture movements” (which is what the UG marketing leans towards) and “designed in Geneva, manufactured on an exclusive contract at a shared specialist in Fleurier” - this feels awfully convenient to just gloss over, don’t you think? To me, this is the difference between owning the means of production and renting them on a long term lease. For years, this was frowned upon; and while I don’t think it ought to matter, simply NOT mentioning it feels a tad deceptive. Again, not a big deal, but it felt like something worth pointing out.

Reality

Stripping away all the marketing and romance of UG; Kern and Partners Group bought a dormant IP for ~ CHF 60m in December 2023 - basically a trademark and a few decades of accumulated collector reverence that other people’s enthusiasm paid for. They commissioned bespoke movements from a specialist who was already doing this kind of work for the rest of the industry. They then walled the operation off in Geneva to protect it from association with the Breitling ‘mass market’. Then they set entry price at CHF 14k-ish, which is high enough to avoid the bloodbath segment between CHF 5–10k and low enough to leave room for the complications to carry decent margin on top. Kern even assembled an advisory board to stop them embarrassing themselves on the initial execution. And now, they have launched several collections at once so the market couldn’t file the brand under any single heading before they’d finished showing their hand.

This is, by any reasonable measure, a good trade on the financial side. Partners Group took Breitling from a CHF 800m-ish valuation in 2017 to around $4.5bn by late 2022, and the UG acquisition is a natural extension of that strategy. That is, they acquire dormant equity cheap, inject competence in operations, and let the multiple expand over time. The watches don’t have to become the new Vacheron for this to work; they just have to become something that justifies a valuation materially above CHF 60m in the next private equity exit cycle, and that’s a much lower bar than the marketing implies. But then again, Breitling’s own valuation got slashed earlier this year… so it’s not all rosy.

Three scenarios for the next few years

Knowing they use LTM movements gives us another way to think about where this goes - as opposed to relying solely on their marketing.

The first scenario, however optimistic it may sound, is that UG executes on what Kern thinks it could become. Volumes may grow slowly into the low thousands, and the relationship with LTM blossoms because LTM has every reason to protect this rather prestigious contract. The complications may even ramp up, the brand’s average selling price may drift upward into the CHF 25–35k zone, the Couture tier does what the Couture tier is supposed to do, and in ten years UG is a credible mid-sized high-end house sitting somewhere in the Lange-to-JLC band. This is the version where Partners Group get a respectable multiple on their money, and everybody wins, more or less, even if the people who bought CHF 14k steel Polerouters in 2026 don’t necessarily feel rich in 2036.

The second scenario is that the market doesn’t reward the launch pricing. The entry point pricing turns out to be too high for what most people actually want from a Universal Genève, given the brand has been invisible for decades and the fanbase was built around cheaper vintage stuff on the secondary market. Sell-through will then soften at full retail, and prices on the secondary market will go the way of most revival launches - i.e. down! Kern will adjust, trim the range, lean harder on the complications and the Couture tier where the margins are more defensible, and Gallet might pick up more of the volume hole than he will ever admit. This is not a disaster scenario per se… it would be more of a normalisation scenario.

The third scenario is some sort of convergence. Over time, it might be that the operational difficulty of running two separate movement programmes (UG via LTM, Breitling via its own manufacture) starts to cause headaches. Maybe LTM gets acquired by someone, maybe it raises prices, or worse, they become capacity-constrained. Or, maybe Breitling’s manufacturing evolves enough to suit or accommodate UG - even with minor modifications. And who knows, perhaps Partners Group (or Kern himself) decide in a few years that the overhead of keeping UG separate, just isn’t worth the cost.

In any of these worlds, UG will start looking more like a sister brand to Breitling than a peer to Lange, and the brand will then settle into something closer to what IWC became under Richemont. Essentially, it’s a mostly-competent, somewhat successful brand (ish!), but it’s no longer competing for the affection of the collectors who revered the original UGs in the first place.

Wait and see

The open question at this point is which way things drift from here. If the entry-level Polerouter holds its price on the secondary market over the next year or two, Kern will have pulled off a difficult feat, and scenario one is firmly in play. If it softens, scenario two will unfold; and you won’t need a spreadsheet to work out which one it is.

After that, it’s largely a question of what happens with Gallet (launching at the end of August or beginning of September, per Kern). If it stays in the entry tier where it was announced to be aimed at (i.e. “accessible” Sellita-powered stuff integrated into Breitling’s distribution) then UG gets to keep the high-end lane all to itself. But if Gallet starts creeping upmarket, or if UG starts “integrating” more and uses Breitling’s movements for anything other than the chronograph, that’s the third scenario - the convergence. Worth watching, but nothing dramatic - these are somewhat slow movies which will play out over a couple of years.

The rest we can mostly ignore; a lot of the noise around revival launches is just that… noise! To be clear, none of this is a prediction that UG will fail. Kern has earned the benefit of the doubt roughly three times over. The products, at least as far as early signs go, seem to be good. The advisory board did its defensive job, the design discipline is clear to see, the movements (regardless of where they’re made) also seem to be a solid effort - including the absence of a microrotor, which per Velociphile, is an upgrade. The brand probably has a future, so the only outstanding question is how successfully it permeates the market.

To me, all three scenarios are fine for Partners Group, which is perhaps the whole point of this approach. Given the acquisition price of CHF 60m, there’s probably no “disaster” outcome on the cards; if anything it’s only a range of good-to-excellent outcomes. This means the interesting question has nothing to do with financials; it’s more about whether the collectors who spent all these decades keeping Universal Genève’s name alive are going to recognise the brand in a decade - otherwise, they’ll look at what Kern has placed in the display cases and decide to go back to hunting vintage instead.

🥽 Nautilus - the 50-year-old porthole

Given we’re in 2026, many in the watch industry are eagerly awaiting Patek’s news regarding the Nautilus 50th anniversary this year; so far, I’ve seen no indication that anyone knows what our boy Thierry Stern is going to do to celebrate.

I suppose the last sentence contains a lie; everybody thinks they know what Stern will do. I’ve seen a bunch of opinions all over the internet... Some Chinese-language leak accounts have supposedly listed some new Nautilus reference numbers1. The speculation market aside, consensus view for now is that Patek will release something in precious metal, and there will be no steel successor to the 5711. I’d be inclined to agree, because “Cubitus”… duh!

Anyway, before we move on to what’s coming, I think it’s worth looking back on how we got here. The Nautilus story is in fact one of the wildest ones in all of watchmaking, and a surprising amount of it is not well-known. If you’ve been collecting for a while, you probably know the broad strokes, and if you’re newer to all this, you might only know the watch as “that steel Patek that costs more than a house” without really understanding the ‘why’.

So first, I will attempt a brief history, and I want to stress ‘brief’, because people far smarter and more dedicated than I am, have already produced some epic scholarship on the Nautilus (more on them later). What I’m trying to do here is give you the story arc, flag a few bits that are surprising or underappreciated, and point you toward the deep-dive resources if you care to dive deeper.

This reminds me of something… you can think of this as the map, not the territory.

Napkin drawing

The origin story of the Nautilus has been told so many times that it’s basically mythology at this point. It’s 1974 at the Basel Trade Fair, and Gérald Genta had already designed the AP Royal Oak two years earlier - plus the Universal Genève Polerouter and Omega Constellation “C” before that. He’s sitting alone in a hotel restaurant, and across the dining room, a table of Patek executives are having dinner. Genta, apparently seized by a burst of inspiration, grabs a napkin and asks the waiter for a pencil. J.C. Biver tells a fun story about Genta’s inspiration for the design of the Nautilus:

In roughly five minutes, while watching the Patek guys eat, he sketched the foundational lines of the Nautilus. Five minutes for a design that, fifty years later, would sell for $7.56 million at auction. Not too shabby eh.