SDC Weekly 144; Thierry denies what Thierry is doing; Grand Feu, a week later; Audemars Piguet’s Ra Tourbillon

Swiss Watch Industry (FHS) March Update, Lange manipulation at auction, Timothée Chalamet takes a stake in UJ, Tudor’s Secret Collector Event, Hans Hilfiker, Bespoke Glasses, Duck-Rabbits, and more!

🚨 Welcome back to SDC Weekly!

Admin note: We asked the Unofficial Editor to check this draft, but he’s reading about Egyptian sun gods today. He told us he’d Ra-ther do literally anything else. Please tap the title of this post or click here to ensure you read the most recent edition, which may include corrections made after publishing.

If you’re new to SDC, welcome! When you have some time, check out prior editions of SDC Weekly here, or find enlightenment in the archive here.

Estimated reading time: ~40 mins

📉 Swiss Watch Industry - March Update

Our favourite federation has dropped the March numbers, and per most reports, everything seems stable. Q1 exports came in at CHF 6.2 billion, up 1.4% (YoY) on Q1 2025 (though March itself was down 1%.) After what we saw in 2025, ‘stable’ is the closest thing to a win you could get, I suppose.

That being said, the rankings do need some sort of health warning. France appears in second place this month with a 72.4% jump, and that isn’t real demand - the FHS itself flagged it as ‘re-exports to other destinations’ as opposed to legit growth in a new market. This seems to have started in December 2025 (when France went up by 50.9%) and has continued every month since.

The simplest explanation is probably some sort of post-tariff logistics rebalancing; brands pushed inventory into the US ahead of the 39% tariff in 2025, then watched US shipments collapse, and then started shipping again once the rate fell to 15%1 in December. As the GS Guy mentions in the comments - the routing through France does nothing to change the US tariff rate - tariffs follow country of origin, not country of dispatch… which means the French routing is about something else (logistics consolidation, VAT or corporate tax optimisation?).

Nobody is willing to name names, but the suspicion is that this is partly a Richemont consolidation play. Cartier is HQ’d in Paris and controls roughly 8.7% of the Swiss watch market by retail value, so French logistics for non-US destinations would make obvious sense. Tariff arbitrage on third-country shipments is also possible - the EU has more favourable bilateral trade deals than Switzerland (with markets like India and Mexico), which means routing via France can amount to lower import duties at the final destination (compared to going direct from Switzerland). If we strip out the French anomaly, March looks more like a 3-4% decline than the headline 1% drop.

There’s another interesting story in the price segments; watches above CHF 3,000 at export (which covers most luxury watches you’d recognise) were down 0.5% in March and basically flat across Q1. This is the segment that has driven essentially all the industry’s value growth for a few years now. The Morgan Stanley/LuxeConsult report in February said that watches retailing above CHF 50,000 accounted for 89% of total industry growth in 2025. If the upper end is flat, this would mean the engine has conked out.

What kept the headline numbers respectable here is volume at the cheaper end. Steel watches were up 5.8% in units but down 9% in value, which means average steel watch values fell sharply. Either brands are shipping fewer Subs and more Hamiltons, or there’s destocking going on – but it’s probably a bit of both.

India crossed into the top 15 (+56.6%), and Mexico also continued its climb (+16.4%). UK exports were up +3.2% to make it the second biggest legit market (France being hub-exports and not real demand) behind the US for the month. The report says:

Over the entire first quarter (+1.4%), several major markets appear to have reached the bottom of the wave, including Japan (-0.4%), Hong Kong (-0.8%), and China (-0.7%).

This is being measured against the same period in 2025 (which was rough!). Greater China was down 9% in 2025 and down 23% in 2024. So Q1 2026 is better described as “still declining, but more slowly than before, and from a very low base.” I’m not sure I would call this stabilisation - what is fair to say is that the slope is flattening, but the level is still falling. The reason it looks “near flat” is that there’s not that much further down to go after two years of mega drops.

Anyway, Saudi Arabia (-16.1%) and Qatar (-24.8%) seem to show the effects of war in the Middle East… but UAE somehow held flat at +0.7%, which defies logic.

I think this is because UAE is the regional distribution and logistics hub for a large chunk of the Gulf, so the FHS export figures for UAE probably include inventory that is eventually sold to buyers in Saudi, Qatar, Bahrain, Oman, and even to other regional and Indian visitors who shop in Dubai.

In essence, the war is impacting the home market economies in Saudi and Qatar, but the UAE’s hub status and diversified consumer base seem to be insulating it. I do think that if tensions get worse, UAE could probably absorb even more redirected business from its neighbours, the same way it absorbed Russian capital after 2022.

Most of this stuff ends up being “insights from hindsight” because who knows what any of this means in the moment. In Q2 we will see most W&W 2026 novelties start hitting boutiques and the post-W&W ordering cycle will kick in. For now, I guess the situation is best described as fragile but stable.

🤔 Thierry denies what Thierry is doing

A few weeks ago, I argued that the Beyer acquisition was not really a one-off sentimental move, and more like Patek doing the same thing Rolex did with Bucherer, but subtly - just a steady slide from wholesale toward DTC.

Thierry Stern would like you to know that he disagrees.

He spoke with Andrea Martel at NZZ for what reads like a polite scolding of anyone (hi) who has drawn the Bucherer comparison. “We don’t go the way of Rolex with Bucherer and become a dealer ourselves”, he said. “Our focus remains watchmaking.”

Straight face

I have read the interview at least 3 times and I still can’t work out how Stern squares his words with his actions. He has just bought a 266-year-old multi-brand retailer, is converting the entire 600-square-metre store into a Patek-only Salon, will lay off about 35 staff in the process, and is opening his fourth directly-owned door in a city he describes in the same interview as “perhaps even more important” than Geneva.

If that is not ‘going the way of Rolex’, it is a pretty good impression of it.

What Stern probably means is that they are not buying an entire 100-store retail group in one go. That’s fair enough. The pace is obviously slower and the perceptions matter to him. But for anyone standing on the sidelines, the direction of travel is identical and the destination is the same - more brand-controlled retail, fewer multi-brand doors, and more direct relationships with collectors plus the data that comes with them.

The difference is in how it is being portrayed; Rolex announced a deal, and Patek is telling us, with a straight face, that nothing is really changing. 🤷♂️

Gübelin exit

The most consequential part of the interview for me, is when he is asked about Gübelin (which sells Patek in Zurich and is, per Stern’s own description, ‘directly opposite our future salon’), he said “in such a small space, this hardly makes sense.” He then walked it back with a polite line “the future of our cooperation with Gübelin in Zurich is currently the subject of discussions.”

To me, that is their death warrant; Patek’s owner has said, on the record, that two Patek doors across the street from each other do not make sense, and one of those doors is his own - so which one do you think is going to close?

I noted before that the Beyer conversion would have second-order effects on Zurich’s retail mix, and now we know what the first one looks like. Gübelin will likely lose its Patek allocation in Zurich, which is a decent chunk of revenue for a retailer that has been a Patek partner for decades. Whether the global Gübelin-Patek relationship will survive is a separate question, but the Zurich part is likely over.

Who paid for the tariffs

Stern also admitted something else; the US slapped tariffs on Swiss watches, and then those tariffs fell from 39% to 15%. Patek raised global prices by 4% on 1 February for materials cost, and US recommended retail prices ended up 8.6% lower than where they started.

So how did Patek absorb the original tariff hit without raising end-customer retail prices? Stern told NZZ, plainly, “we have reduced the dealer margin to compensate for the tariff-related price increases.”

So when the tariffs were at 39%, Patek’s US dealers ate the cost and end customers paid the same. Patek protected its brand image and its retail prices, and the dealers got squeezed. Now that the tariffs have come down, Stern doesn’t say whether the dealer margin has been restored, or whether Patek has just pocketed the spread.

I don’t know the answer, but ask yourself; if you were running Patek and you had just taken a chunk of margin off your dealers, supposedly only until the tariffs eased, and the retail prices the customer pays were now lower than they had been before… would you give that margin back? Or would you keep it, point to the lower retail prices as evidence of consumer-friendly pricing, and let the dealers absorb that loss?

If you combine this with the Beyer conversion, the picture starts to look quite consistent. Make the multi-brand model less profitable, and wait for succession or commercial pressure to take its toll. Then step in when the family runs out of options and convert.

Slow-motion

A few other lines in the interview fit the narrative; “We don’t want to open up new markets. We don’t have enough watches for that”, is the Patek line that has been recited since at least 2010 and that is somehow always true regardless of capacity. “Our goal has never been to make as many watches as possible”, which is fine, but is also the only acceptable thing to say given that they have been stuck around 75,000 watches a year for ages and seem to be hitting a wall on production.

The capacity-constrained, growth-isn’t-the-point framing is also the perfect cover for the retail consolidation. If you cannot make more watches, you do not need more dealers. You probably need fewer, but better placed, and ideally ones you control yourself. Every sentence Stern utters about constrained production is also really just a sentence about why fewer doors and more brand-owned Salons make more sense.

From where I’m sitting, Patek’s strategy looks pretty smart. Doing it slowly and politely, and continuing to tell everyone the third-party retailer model is sacred, is actually quite shrewd. It lets you keep the relationships with the dealers who still matter, while also relying on them less over time.

We should probably stop letting the brand tell us what is happening and just observe what they actually do. Stern says they are not going the Rolex way. Maybe… but every action of the last few years (shrinking from 400+ points of sale to under 300, opening fourth and fifth and likely sixth directly-owned Salons, acquiring a long-time partner the moment a succession crisis offered an opening, squeezing dealer margins to absorb policy costs) is a step on the same road Rolex took. They are just walking it more slowly, and I suppose with better manners… but methinks Patek ADs should start counting down to a world without Pateks to bundle.

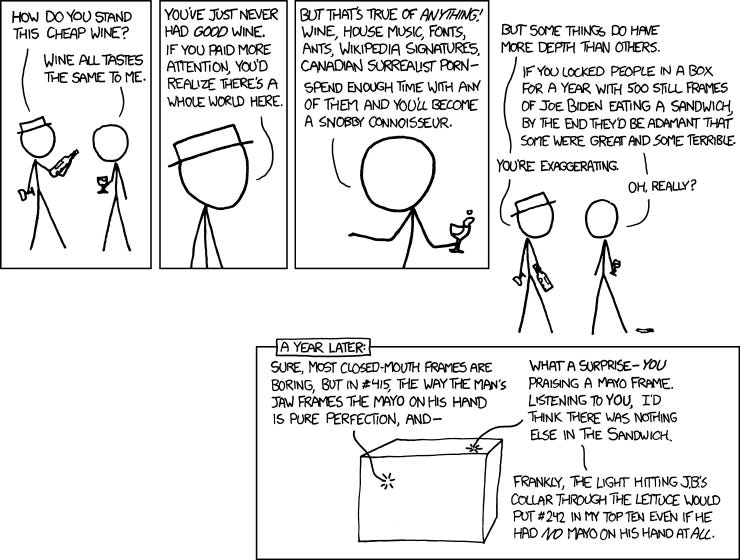

🔥 Grand Feu, a week later

When Rolex launched the new off-catalogue steel Daytona I made the case that they had borrowed the term ‘Grand Feu’ from the rest of watchmaking to label a dial-making process that does not meet the 150-year-old watch industry definition. I still stand by that... looks like Fratello agreed with me as well. Hot off the press… Jack Forster also covered it yesterday and concluded, very appropriately I might add, with this XKCD comic:

With that, we shall continue with, to borrow Jack’s words, “the endless pleasures to be derived from the human tendency to elevate minor points of distinction to the level of doctrine.”

More than a few people pushed back in the comments on my Grand Feu post; the point, roughly, was that the new Rolex ‘Grand Feu’ dial is simply nicer to look at than the metal-substrate enamel dials you have seen in person. I have not held a new 126502 myself, only looked at photos, and enamel tends to photograph badly at the best of times… so I can’t really referee this. But let’s assume you are right, and that the new Rolex dial is the prettier object under neutral lighting.