The Art of Divergence - Greubel and Forsey Split

Stephen Forsey's termination, the 51/49 ownership problem, potential sale rumours, and what collectors lose when a founder gets pushed out.

I tried to ignore the noise, but the Richter (drama) scale went off the charts this week. If you’ve been reading SDC for a while, you know I hold Greubel Forsey in fairly high regard. We covered their production economics in SDC Weekly 105 and the nuances of their Hand Made activities in SDC Weekly 115. I’ve also been fortunate enough to call the current CEO, Michel Nydegger, a friend - this was before he became a CEO and stopped taking my calls immediately 😂. All joking aside, I am clarifying this friendship to allay any concerns about biases - I’m just after the facts, and Michel is running a company… everyone’s doing their thing. As we often discuss here, we see the world as we are, not as it is, and right now (perhaps as it always has been!) the world of Greubel Forsey looks... complicated.

Estimated reading time: ~ 9 minutes

Public Statement

It’s rare for the Swiss watch industry to air its dirty laundry in public. Usually, departures are wrapped in euphemisms like “pursuing other opportunities” or “mutual agreement.” This is, quite clearly, not that!

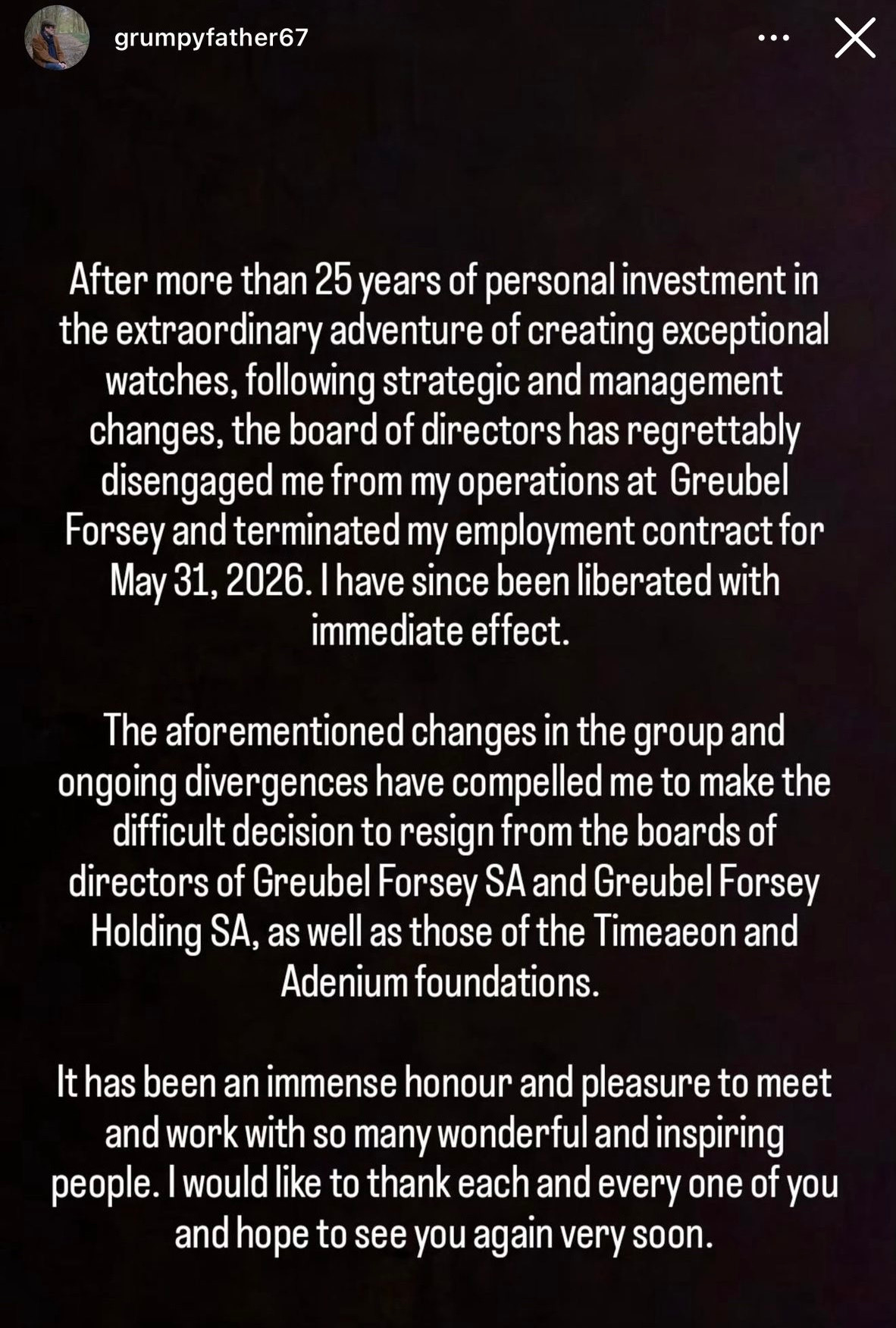

Stephen Forsey released the above statement yesterday via his Instagram and LinkedIn pages, and it was as polite as it was devastating. After more than two decades building one of the most prestigious names in independent watchmaking, he has, apparently, been removed from the building.

“After more than 25 years of personal investment in the extraordinary adventure of creating exceptional watches, following strategic and management changes, the board of directors has regrettably disengaged me from my operations at Greubel Forsey and terminated my employment contract for May 31, 2026. I have since been liberated with immediate effect. The aforementioned changes in the group and ongoing divergences have compelled me to make the difficult decision to resign from the board of directors of Greubel Forsey SA and of Greubel Forsey Holding SA, as well as those of the Timeaeon and Adenium foundations.”

There’s a ton of nuance in here… shown in bold text. Even with the most generous interpretation, this would appear to be a founder being ousted from the company that bears his name.

This post draws on reporting from WatchPro and Miss Tweed, linked in the footnotes below, alongside my own coverage and direct conversations1. Before we dive in, let’s clarify what we’re working with… because it’s important to separate facts from opinions.

Facts

Stephen Forsey says he was “disengaged” and “terminated” by the board, effective 31 May 2026, but with “immediate effect” seemingly his own choice to accelerate the process.

He has resigned from the boards of Greubel Forsey SA, Greubel Forsey Holding SA, and the Timeaeon and Adenium foundations

He remains a shareholder with 49%; Robert Greubel holds 51%

Robert Greubel has not commented publicly

Michel Nydegger told WatchPro there are no sale discussions happening

The company describes Forsey’s departure as a “logical consequence” of gradual withdrawal from operations

Greubel Forsey produces around 200 watches annually with approximately 135 employees

The company generates roughly 40-50 million CHF in annual revenue

Unverified / Unsubstantiated

Industry sources suggest the company may be testing buyer appetite

Former AP CEO François-Henry Bennahmias reportedly looked at the brand

Various characterisations of the interpersonal dynamics between the founders

Unknown

What specifically the “strategic and management changes” and “ongoing divergences” were

Whether a sale is actually being contemplated by either founder

What Robert Greubel thinks about any of this

What the future holds

One could argue we should just leave it here… but where’s the fun in that?!

The 51% Problem

Robert Greubel controls the company with a 51 percent stake and Stephen Forsey owns the remaining 49 percent. In the boardroom, I guess 51% might as well be infinity. In this case, it seems to mean that one person can outvote the other on everything that matters like board composition, strategy, hiring, firing, and maybe even selling. The 49% holder obviously has a massive economic interest but as it appears here, very limited ability to shape the outcome if the relationship sours. It is perhaps easy to see how that dynamic might create tension over a quarter century.

I met Stephen Forsey back in 2018 (or maybe 2019) when he visited London for a Redbar meet-up in Knightsbridge. He is an absolute gentleman; soft-spoken, affable, and in love with watchmaking at a cellular level. For two decades, he was the brand’s primary ambassador, often seen in his trademark braces, connecting with collectors.

As for Robert Greubel … I did see him on Wei Koh’s TV show, but that’s about it. Some people do prefer the workshop to the spotlight (Stephen McDonnell seems like one of those people as well - but I digress). This is not a criticism at all - more of an observation about how differently these two founders approached their public roles.

Anyway, the company’s official response paints Stephen’s departure as the natural conclusion of a gradual withdrawal from operations. Stephen’s statement describes being “disengaged” and “terminated.” These accounts are difficult to reconcile, and in reality, we may never know which account is closer to the truth.

Strategic Whiplash

To understand the “divergences” Stephen mentioned, we need to look at the strategic rollercoaster the brand has been on. Richemont bought a 20% stake in 2006, back when the conglomerate was collecting small independents. Richemont then sold it back to the company in 2022, and that so-called buyback was supposed to herald a new era of freedom and founder control.

Calce Era (2020-2024): Antonio Calce arrived as CEO with ambitious plans, and to be more specific, his strategy was best described as aggressive expansion. Production would more than double towards 500 watches per year, up from roughly 100. The average price point would drop from around CHF 500,000 to CHF 250,000. The dealer network would be cut dramatically, and replaced by directly-owned boutiques in key cities. Construction actually started in 2023 for a massive extension to the La Chaux de Fonds atelier which was supposed to nearly triple its footprint.

Then the post-pandemic watch market somewhat normalised, and the hysteria that had driven waitlists and grey market premiums cooled off. Calce was out by May 2024, the atelier extension was mothballed, and the 500-piece dream was put to bed.

Nydegger Era (2024-Present): Michel Nydegger, formerly marketing director, took over as CEO. In a recent WatchPro interview, he said production is capped at 200 pieces because the company no longer feels the need to chase volume, and they prefer to “walk before they run” on distribution.

This pivot back to exclusivity and restraint is precisely what I hoped would happen when we discussed the brand in SDC Weekly 105. The production economics at 200 pieces actually work quite well. With 135 employees generating 40-50 million CHF in revenue, they’re essentially running a horological research institute funded by ultra-luxury watch sales. It sounds a bit mental, but it kinda works.

The confusing thing for me is if the brand pivoted back to the exclusivity that Stephen Forsey likely championed, why push him out now?

For Sale?

Industry sources suggest Greubel Forsey may be testing buyer appetite. We all know François-Henry Bennahmias seems intent on building a portfolio in high-end watchmaking… I understand his first choice was DeBethune, but Danny Govberg supposedly keeps changing his mind and they can’t seem to reach a deal on DB (doesn’t mean it’s off the table). Anyway, FHB reportedly had informal conversations about Greubel too. When WatchPro asked Michel Nydegger directly whether there were discussions about selling the business or taking on new investment, he replied that there were no such talks and they weren’t looking to have any.

You might be sitting there thinking I am trying to defend a friend - but he knows better than anyone, I am forced to stay objective and honest here, otherwise SDC would lose all value. So, who should we believe? Well, I see no reason not to take Michel at his word, and I think the reality is that both statements can be true!

A CEO can honestly say “we are not in sale discussions” while a majority shareholder may still be testing the waters through intermediaries (but not formally). Nydegger runs the company day-to-day; he might not be privy to every informal conversation Robert Greubel has with potential suitors. Or… the rumours could simply be wrong. We have no way of knowing, and if they were looking to sell, do people expect Michel would just come out and say it just because I or anyone else asked? Why should he?

Anyway, what we do know is a 51/49% ownership split with fundamental disagreements about strategy will no doubt create complications. If one founder wants to sell and the other wants to keep building movements and coming up with new mechanical architectures, that kind of divergence will be difficult to bridge. If Robert wants liquidity and Stephen doesn’t (or vice versa), you can see how the partnership instantly becomes untenable.

The company could be worth north of 100 million CHF… It’s also a valuable asset with its own movement manufacturing capability and more than 60 patents - that’s the sort of thing which doesn’t grow on trees.

What Collectors Lose

Why do people buy an MB&F, a Kari, or a Romain Gauthier piece? I’d say it has a lot to do with getting to know the watchmaker. The personal relationship (or some connection to the creator) is part of what justifies spending stupid amounts of money on an independent watch. If you want a faceless brand, you buy a Rolex or something.

Stephen Forsey was that connection for two decades; collectors adored him, and he could explain the philosophy behind a double tourbillon in a way that made you feel like you understood something profound about timekeeping. He was, for lack of a less cheesy term, the soul of the brand.

Apparently, if you email Stephen Forsey at his company address today, you get an auto-reply directing you to Michel Nydegger. It’s a cold end to a partnership that began with the motto “The Art of Invention.”

Looking Forward

The company says 2026 will be the final year for several existing calibres, followed by an entirely new collection. Business continues as usual for now… Greubel Forsey holds more than 60 patents, and their reputation for finishing is largely undisputed. The watches themselves remain extraordinary objects, and none of that goes away because one founder has departed.

But from where I’m standing, something intangible has indeed been lost. The name “Forsey” will remain on the dial, but Stephen Forsey won’t be the one handing you the watch, explaining its ingenuity, making you feel like you’re joining a fellowship of rich nerds who value what they’re buying beyond just “a wildly expensive watch” - everyone knows you buy a Richard Mille for that. A GF watch is supposed to be about something more than just flexing!

I sincerely hope the brand finds its footing. As I said, I like Michel, and I have immense respect for what Greubel Forsey has achieved. Having said that, after reading Stephen’s statement it’s impossible not to feel sadness over a creator being separated from his creation.

Stephen said he has been “liberated” and I sincerely hope he takes that liberation and does something extraordinary. He is 58, which is absolutely not “retirement age.” Given his reputation and connections, I am sure he won’t be short of opportunities. If I were a brand looking for someone who embodies the spirit of haute horlogerie, I’d be calling him immediately.

In fact, I actually suggested to Jean Arnault that he partner with Stephen to create Naissance d'une Montre 52 - that would be cool because I trust Stephen would bring some proper watchmaking sauce to the table, and Jean can basically afford to bankroll any wild ideas Stephen comes up with. Wouldn’t that be epic?

Watch this space. Literally.

Edit: 4 Feb 2025: A subscriber pointed out that I failed to mention Michel Nydegger is Robert Greubel’s stepson, and that this fact might suggest the entire story is one of succession planning and ‘keeping it in the family’.

I was under the impression that this is common knowledge, so for the avoidance of doubt, I am adding this information here. Some have extrapolated the underlying intent of all these maneuvers as a scheme to turn Greubel Forsey into a Greubel ‘family business’ - this is of course, a matter of opinion. Feel free to factor this in to your calculus if that makes the most sense… it doesn’t really change anything I’ve written above.